Buzz words like ‘bitcoin’, ‘blockchain’, and ‘cryptocurrency’ are everywhere. Blockchain has begun to reshape business models across many sectors. Blockchain innovation has started to impact government infrastructure, citizenship, voting, and health. Smaller countries with more cohesive power have already taken dramatic steps to decentralize their infrastructure and systems.

So, what is a blockchain, and how does it work?

Here is my effort towards trying to explain what blockchain is in brief.

What is Blockchain really?

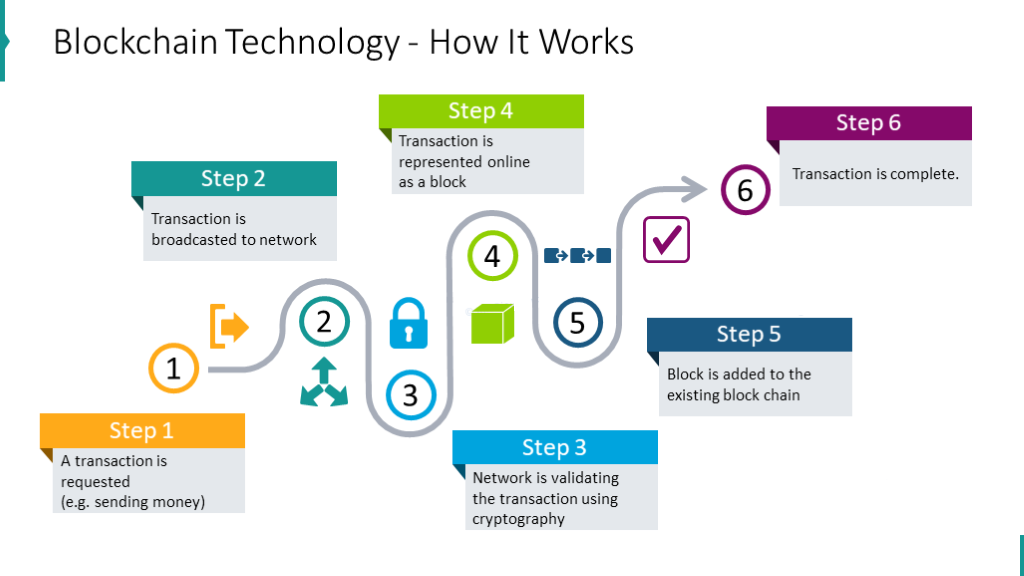

We could define it in a simplified way as a chain of data blocks linked by cryptography and chronologically . Each block is linked by a cryptographic hash to its previous block, so that the data that has been entered in the chain cannot be modified again.

This chain is created through the different participants that make up a Blockchain network. Any record in the chain can be consulted, but not deleted or modified as we have previously commented, and to add a new block to the chain, a consensus is required among the network participants.

With these characteristics, the following properties are derived:

- Immutability : when data is recorded in the chain it is irreversible.

- Transparency : all blocks are visible and can be consulted.

- Trust : Thanks to the distributed consensus with which new blocks are created, trust is guaranteed in the process of creating them.

Blockchain in even simpler terms.

For all of the hype around blockchain, most businesses are barely tinkering with it right now – if they’re doing anything at all.

Change is coming: Research firm IDC, among others, predicts booming growth, expecting worldwide spending on blockchain-related spending to hit $9.7 billion in 2021, up from around $2 billion in the year 2018-19.

But what’s the hold-up for IT leaders? Gartner points to one reason in its survey results: Blockchain engineering skills are hard to come by and, as a result, are expensive.

There’s another issue: Many people still don’t understand what blockchain is. Moreover, people who do understand it sometimes have a hard time explaining it succinctly, especially if they have to do so in non-technical terms that a wider audience can understand.

A lack of internal knowledge and a lack of affordable talent on the open market, “pretty much [rules] out any near-term blockchain project. Presumably, that will change.”

The talent issue is going to take some time, so we’ll set it aside for the moment. But we can roll up our sleeves and try to help people better understand blockchain in clear, relatively easy terms. one of the easiest is given by Tim Kulp.

The School Lunch explanation

Tim Kulp, director of emerging technology at Mind Over Machines, serves up “School Lunch,” an explanation that, quite literally, a second std kid would be able to understand:

Imagine a school lunch table with a bunch of kids sitting at it. Two kids want to trade lunches. Kid A says: ‘I’ll trade you lunch if you have a cookie’ to Kid B. Kid B states that he does have a cookie and the two trade lunch.

“Imagine a school lunch table with a bunch of kids sitting at it.”

As the kids trade lunches, the Principal comes over and asks: ‘What’s going on here.’ At which point all the kids at the table speak up and say Kid A traded lunch with Kid B.

This simple story outlines the basics of blockchain. Kid A and B are ‘participants,’ also known as actors, in the blockchain. Lunch is an asset. Trading lunch is the transaction. Whether Kid A’s lunch contains a cookie is a smart contract. Finally, the Principal’s review is the consensus to approve/validate the transaction.

[To summarize,] blockchain is the process of participants engaging in transactions around assets. Consensus is used to validate the transaction and smart contracts are used to set parameters around the transaction.”

No, Kulp’s not scoring points for the briefest explanation. But it’s how he explains blockchain to non-technical people who don’t really need a deep dive into things like cryptographic signatures, how consensus works, or the architectural design of a blockchain system.

Where is the blockchain saved?

Each participant of the Blockchain network can keep a copy of the chain , so that there is no centralized point where the blocks are stored , leaving them fully distributed within the network. Every time a new block is created, it is distributed among all the participants so that they can store it in their local copy. Therefore, Blockchain is considered a form of DLT (Distributed Ledger Technology).

This brings us to another of its most important properties, Decentralization . This prevents a central point of failure as the entire chain is distributed.

With these ideas as a base in mind, we are going to make a brief review of how technology has evolved from Bitcoin until now, since new concepts such as Smart Contracts have appeared as their use became more extensive.

Bitcoin: the origin

When in January 2009 Satoshi Nakamoto registered the first block (genesis block), thus creating the open source Bitcoin network, the first cryptocurrency and the first Blockchain network were born . The objective of this network is to carry out monetary transactions without intermediaries.

Since its inception and thanks to being an open source network, a community of programmers is in charge of its development and evolution . In other words, it is done through the consensus of the community. Later, other cryptocurrencies based on the same concept (altcoins) appeared and disappeared with almost the same speed, but with different objectives. However, they served as a seed for the generation of other Blockchain networks that went beyond peer-to-peer transactions.

Second wave: Ethereum and the Smart Contracts

In 2013 a developer from the Bitcoin community, Vitalik Buterin, proposed leveraging the network to run distributed applications. His proposal was not accepted, so in 2015, together with a group of developers, he launched the first Blockchain network, which successfully implemented the use of so-called Smart Contracts, Ethereum .

Ethereum is also a public, open source network and has its own cryptocurrency, Ether.

The Smart Contracts , on the other hand, is a piece of code that runs on the network Blockcahin, can handle digital assets and implement a number of arbitrary rules. For example, they could be used to establish the rental agreement of a property between several participants, but without an intermediary or central authority as it currently exists with other platforms.

Third wave: new types of Blockchain and evolution

After the rise of Bitcoin, Ethereum and other public networks, new needs began to emerge such as greater privacy, transactionality or scalability . These have tried to be solved by evolving existing networks or creating other types such as private networks or federated networks.

The new types of networks are more oriented to the business world, where the privacy provided by a public network is not sufficient or a certain degree of trust is required among the participants of it.

As notable examples we have, among others: Quorum , based on Ethereum and started by the JP Morgan bank with which it is possible to carry out private transactions; R3 Corda , focused on the financial world and other specific industries; or the Hyperledger project , under the umbrella of the Linux Foundation where different projects have been grouped together, such as Fabric (for permitted networks) or Indy (decentralized identity).

However, this technology is constantly evolving and new protocols and projects emerge every so often.

With this we have made a brief review of what Blockchain is and how it has evolved over the last few years. In the following articles that we will try publishing, we will go into more detail about its operation, important concepts such as Smart Contracts, consensus algorithms and many other topics related to this technology.

Benefits of Blockchain

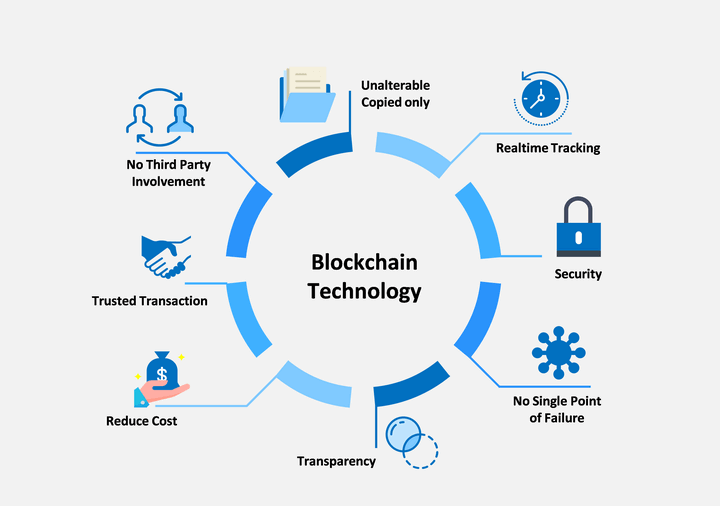

Some of the top features and advantages of blockchain are as below:

- Speeding up transactions

- Blockchain’s verification system has the potential to enable near to or real-time processing and settlement of transactions.

- Cutting costs and complexity

- Blockchain can be used to orchestrate and automate interactions with external parties, as well as within your own processes.

- Reducing data duplication

- Blockchain provides a single shared view of the truth in your network, reducing data entry duplication and reconciliation.

- Increasing resilience

- Due to the distributed nature of blockchain, there is no single point of failure. This makes it significantly more resilient than current systems.

Stay tuned for my upcoming posts for more information on blockchain implementations, we will finish this blog by briefly looking at what are the future prospects of this exciting technology.

Prospects

Blockchain technology is relatively new and has not been encompassed in the mainstream industrial sectors. This has resulted in it being neglected for the time being but there has been rapid development in the sector in this year. This has displayed several plausible applications in various fields which are not implemented as the pros of this do not outweigh the pros of the existing models. Will the rapid development of Blockchain Technology and increasing ease of its usage be a tipping point in the technological Industrial Revolution 4.0?

References

[1]. Book – written by Tiana Laurence: Introduction to blockchain technology – The many faces of blockchain technology in the 21st century.

[2] School lunch example from Author :-Kevin Casey ( https://enterprisersproject.com/ )

[3] Images :-

Introductuctory : https://medium.com/@tokenmeister.social/the-cryptocurrency-and-blockchain-revolution-is-coming-42ceb5b2e25b

Blockchain Working :- https://www.infodiagram.com/diagrams/blockchain-diagrams-distributed-ledger-network-template-ppt.html

Benefits of Blockchain :- https://www.sketchbubble.com/en/presentation-blockchain.html